Markets do remain overvalued across the investment part

of the economy and we may see normalisation in some of

these segments.

We remain bullish on equities from a

medium to long term perspective.

Investors are suggested to have their asset

allocation plan based on one's risk appetite and

future goals in life.

|

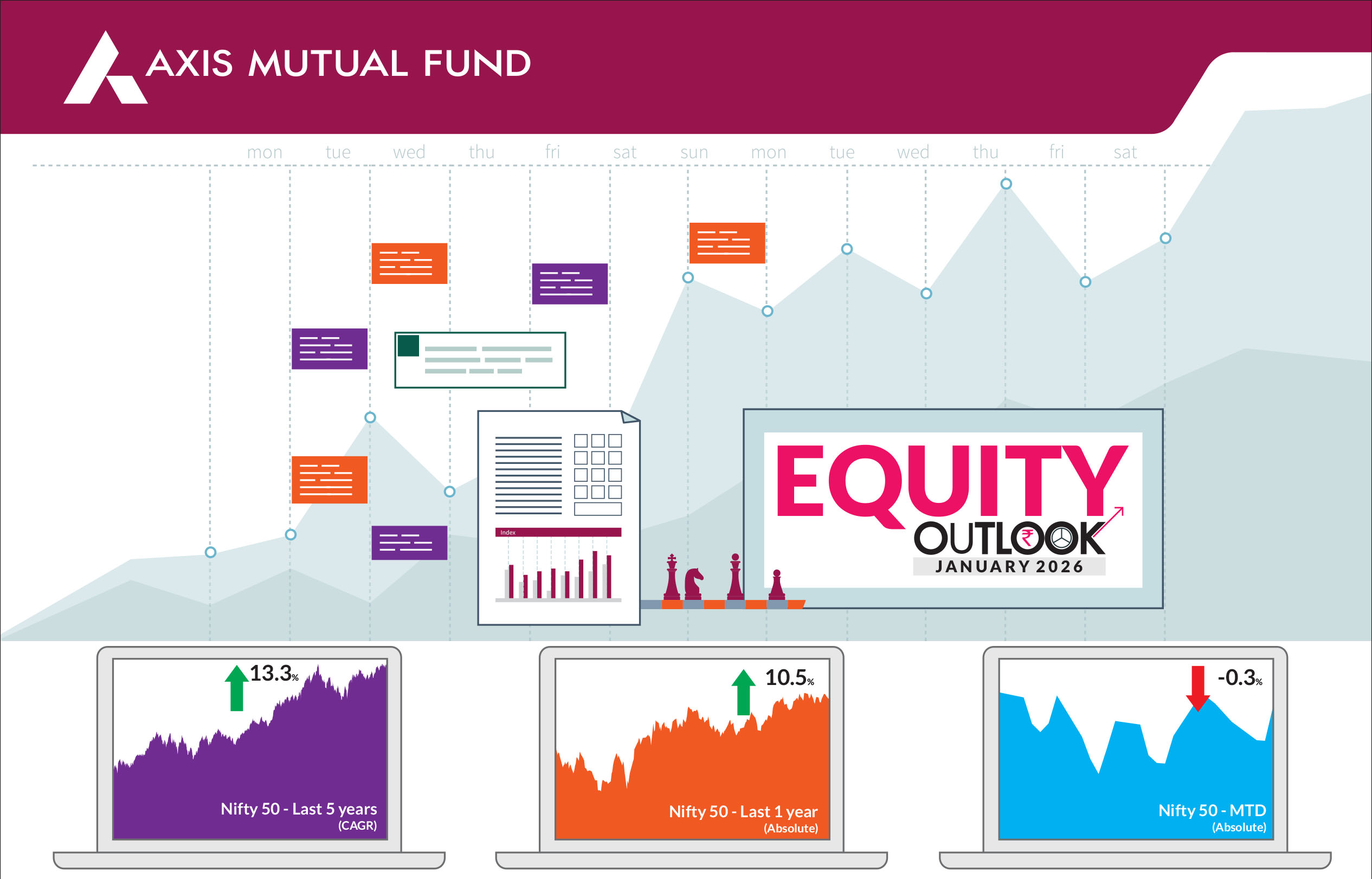

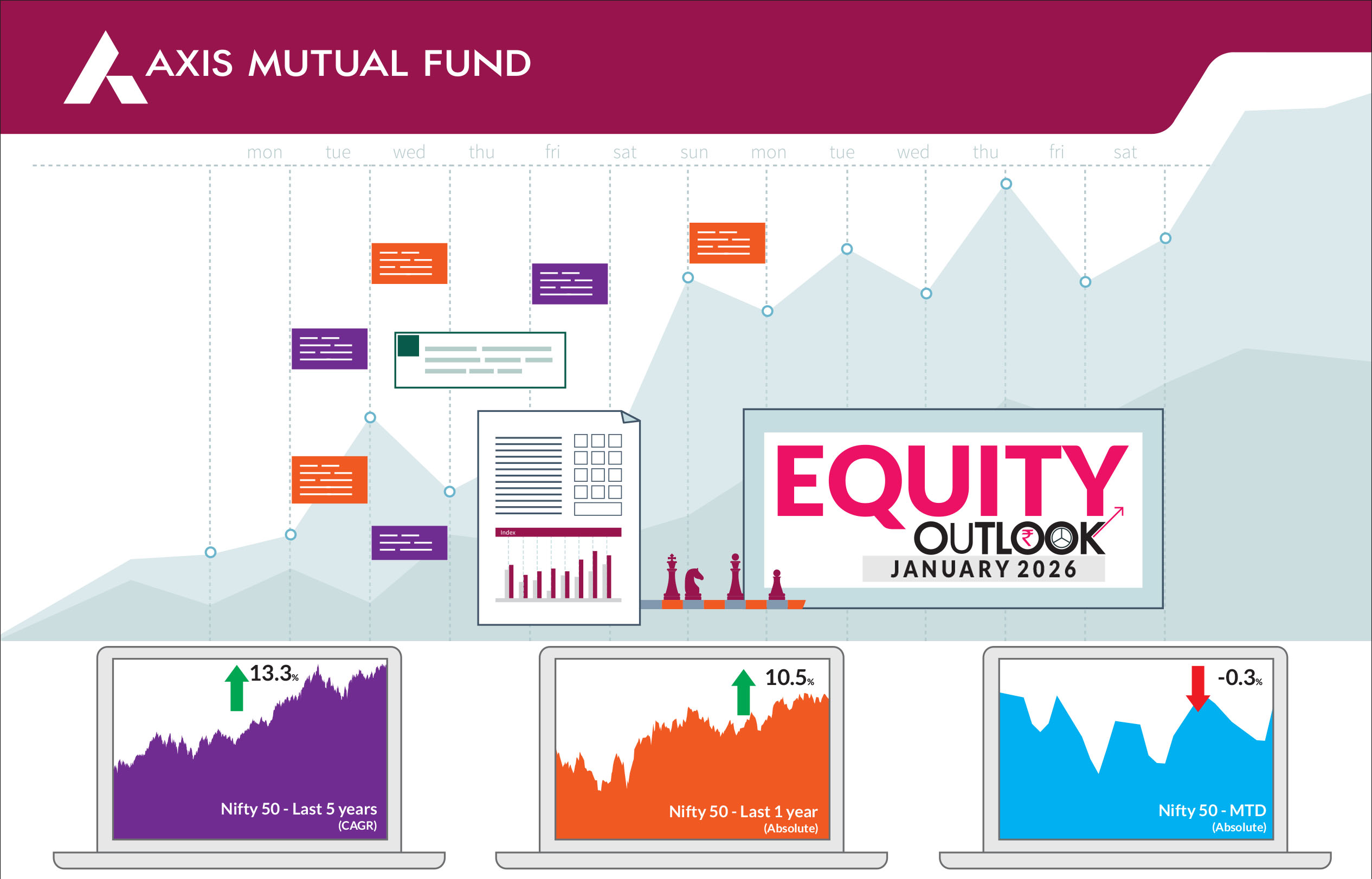

Happy New Year from the entire team at Axis MF! After three consecutive months of positive returns, equities ended the month lower. For most part of the month, equities remained rangebound impacted by concerns over the India-US trade deal. Large caps outperformed mid and small caps. The BSE Sensex and Nifty 50 closed 0.6% and 0.3% down, while the NSE Midcap 100 fell by 0.9% and the NSE Smallcap 100 by 0.6%. On the sectoral front, metals, oil & gas and auto were the top gainers, whereas capital goods, consumer durables and realty were the top losers. Foreign Portfolio Investors (FPIs) sold equities to the tune of US$2.5bn while Domestic Institutional Investors (DIIs) remained supportive with US$8.1bn in equity purchases. Year to date, FPI outflows total US$19bn while the DIIs bought to the tune of US$89.5bn. As we enter 2026, markets reflect the recovery from a challenging 2025. Equities regained their previous highs in 2025 following correction seen in 2024, while valuations, though off their peaks, remain in line with long-term averages. Importantly, India's valuation premium over emerging markets and global peers has narrowed considerably and appears to have stabilized. The earnings cycle seems to have bottomed out, with signs of a sustained recovery ahead. This optimism is underpinned by coordinated policy measures from the RBI and the government-rate cuts, CRR reduction, liquidity infusion, accelerated capex and nearly Rs1.5 trn in GST reductions aimed at boosting mass consumption. Adding to the positive backdrop are easing geopolitical tensions with China and its antiinvolution reforms, while a potential India-US trade agreement could further strengthen sentiment. |

|

A lower tax regime and benign inflation have created a goldilocks environment of

strong GDP growth and lower inflation prompting the RBI to revise growth

forecasts upward. As these measures take hold, India is poised not just to sustain

momentum but to emerge as one of the most resilient economic growth stories

globally. Globally, all countries had a stellar year with India being an outlier. AI was the key theme of 2025 and India did not have much to offer on this theme. The 'Magnificent 7' have accounted for more than half of total market returns, including dividends, since 2023-a rally largely driven by surging optimism around artificial intelligence. |

|

Outlook & Positioning The Reserve Bank of India's accommodative stance, characterized by proactive rate cuts and ample liquidity, has created a supportive backdrop for growth. Coupled with fiscal measures like GST rationalization, tax cuts, MSME support, and regulatory reforms by RBI and SEBI, these initiatives have laid a strong foundation for India's structural recovery. India's macroeconomic stability will be underpinned by fiscal consolidation efforts, benign oil prices, and steady global growth. Domestic consumption demand is expected to remain buoyant, driven by premiumization trends, rural recovery supported by agricultural activity, and fiscal support from state governments. These factors collectively create a favorable backdrop for sustained economic expansion. The resolution of tariff issues between the US and India can help accelerate recovery.Earnings have likely bottomed in India and we could see a broad-based recovery in CY26. Markets expect mid teen EPS growth 2026, with reduced risks of downgrades compared to 2025. Over the 18 months, earnings estimates in India were lowered. However, the picture is looking better over the last three months with positive developments, such as GST rate cuts (key beneficiaries being autos, followed by consumer staples). High frequency indicators are reflecting improvements. Financials, IT services and auto estimates have been stable in the last three months, while construction materials, realty and metals have seen upgrades. The market is expected to continue its focus on high earnings visibility, sustained profitability and structural growth catalysts along with reasonable valuations. While bottom-up stock picks around popular themes remain expensive, underperformers due to slower growth with relatively attractive valuations offer selective opportunities. Stock picking with a focus on growth at reasonable valuations will remain the cornerstone of performance, with a clear preference for domestic-oriented sectors over export-heavy plays. Overall, we maintain an overweight stance on consumption. The positive impact of GST rationalization is seen across consumer discretionary companies who have reported strong festive-season sales. We also remain constructive on other consumer discretionary plays-especially in retail, hospitality, and travel & tourism-which are gaining from strengthening domestic momentum. In automobiles, the trend toward premiumization is expected to strengthen, supported by a pickup in the replacement cycle. Recent consumption numbers and management commentaries suggest that consumption sector has gained post GST rationalization however continuity in revival needs to be seen in coming months. We have increased exposure in financials over the last year as these are wellpositioned to benefit from expected revival in credit demand and improved liquidity conditions. Furthermore, we are overweight Healthcare. We remain underweight in IT given the cautious environment in the US although rupee deprecation and attractive absolute valuations are enticing, relative valuations vis a vis global peers are still expensive. Additionally, we are positive on structural themes such as renewable capex, power transmission and defense. |

Source: Bloomberg, Axis MF Research.